A reminder of Mrs Mummypenny Spending diaries series and what you can expect to read.

A chance to read other peoples spending diaries, a mixture of all sorts of guests, parents, single folk, men and women, older and younger, from all parts of the country. Not only is it interesting to read, it is also something you can learn from.

Other people do great things to save money. Or maybe empathise with, emotional spending, mum guilt (talking from experience here).

The Mummypenny Spending Diaries – Miss Pennymoney

Please note this is not me!! Fiona has chosen a blog name very similar to mine.

I am Fiona, AKA Miss PennyMoney I am a stay-at-home mum and I have spent the last few years trying to find a balance that allows me to look after my children and earn some money at the same time. I have also been in a permanent state of debt since the age of 18 (go to end of this spending diary for my debt story).

I made the commitment to become debt-free last year and set up my blog to document my progress. I’d love to inspire others and share my discoveries along the way. I also share a lot of my progress on my Instagram channel here.

I logged my spending for the whole of July for this spending diaries series and discovered some really interesting insights from it to see where we were potentially overspending.

The Start of My Spending Diary

The first thing I did was to write down all of our outgoings for the month as far as bills, debt repayments and fixed expenses were concerned. Historically, when I’ve put together a budget, I’ve only included these things and then some money for food and fuel.

It’s easy to forget about those little spends here and there that add up. Especially when it comes to buying household items missed at the supermarket, buying the kids a Happy Meal, or paying an unexpected (forgotten) bill that’s popped up.

Splitting it into Categories

In order to really see the spending habits, I’d split a receipt with more than one purchase into categories. This makes things easier to add up and review at the end of the month. For example, with my grocery shopping, I’d split it into food, alcohol and household stuff. At the end of each week, I added up the category totals and put them into a spreadsheet, so I could see how much had been spent on each category per week.

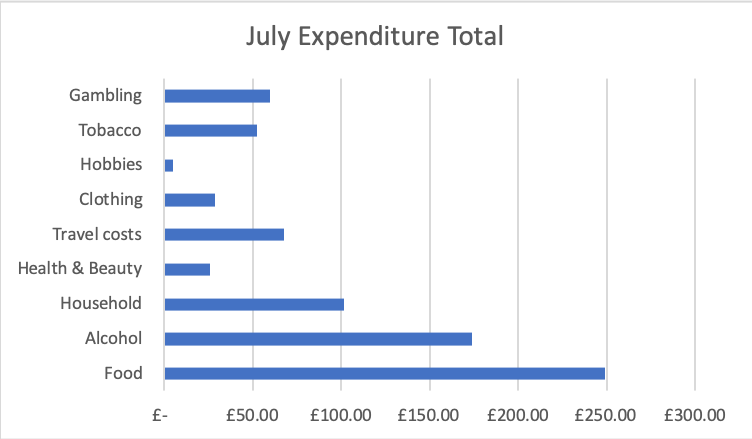

The above image shows our expenditure by category split for the whole month of July. It was a bit of a shocker to see the percentage of income that had been spent on alcohol! We had two social occasions at home at the beginning of the month, which accounted for a large chunk of it. We also bought a barbecue for said occasions, which bumped up our usual household expenditure.

I perhaps should have renamed the ‘gambling’ category. This was actually my husband’s outlay for a football Dream Team he does at work. (To be fair, anything where money is lay to chance, I view as gambling anyway!) The tobacco expense annoys me, but that’s only because I’m not a smoker. And I feel that the amount we spent on alcohol needs to be checked. There are things I’d rather be spending money on, such as some new running shoes!

Essentials vs. Non-Essentials

I love being able to see how our spending is split into ‘Essential’ and ‘non-Essential’ spends. Essential spends for us include food, household items, clothes, travel and health/beauty. Basic human needs – especially food, clothing and essential living expenses – must be met.

It’s also really interesting to see how little we spent on clothes, health/beauty and hobbies, certainly for July, anyway. With our food spend being the highest, it’s also nice to see the total for the month, as this helps with budgeting. I’ve historically allocated £300 to food for the month, although to be fair that’s also supposed to cover drinks and household cleaning products too. As this total is purely for food, I need to revisit our budget. I think perhaps we also need a sinking fund for social occasions!

Next time, I’ll include our household bills in the category splits. I think if you’re on a journey to become debt-free, it’s really helpful to see where bills for some services may be unnecessary.

I hope this spending diary/log has been insightful for you. I’d love it if it inspires you to log and track your own spending. It really is an eye-opener, especially for people who are hoping to change their habits when it comes to money.

Read other posts in the series

Read other spending diary posts here from Bee Money Savvy, Dove Cottage and Thrifty Londoner.

Fiona has also written about her debt-free journey

In 2012, I decided to quit my job and become a stay-at-home mum. Given that I worked in customer service, I effectively worked to pay someone else to bring up my daughter. I had no family to rely on for childcare, so the costs outweighed any reason for going to work and missing out on watching my daughter grow up. So, after a 5-month gruelling full-time return to work, with a 7-month-old baby, I gave up my salary and ‘security’ in favour of motherhood.

Since then, I’d been dipping my toes in and out of the blogosphere and writing in my spare time. It wasn’t until mid-2018 when I was reviewing our financial situation that I had an ‘ah-ha’ moment, and decided to combine my love for writing with my journey to become debt-free. My financial situation wasn’t going to improve itself, so Misspennymoney.com was born.

How did I get into debt?

I’ve been in debt since the age of 18; old enough to apply for my first credit card. Not long after that came a finance agreement for a new car. Then my bank kindly provided me with an overdraft. At that age, I had no concept of what I was doing or the need to plan for my future. Why would I? I was 19, single, living on my own, and having a ball. Until the moment I realised I had a debt problem, and set about trying to tackle it.

I spoke with my creditors and set up payment plans, and after some budgeting (basically just covering my bills), worked out I had £50 a week to live on. That was for food, travel costs, clothing etc and my social life. It wasn’t enough, and I recall days trawling round Netto (remember them?) with my coins in one hand and my shopping list in the other. I remember trying to scrape together enough money to treat myself to a bottle of wine. Or working out that with one onion, a couple of carrots, and a few potatoes, I could make a veggie stew for just a few pence.

Despite my attempts to get out of debt, my life went on a bit of a cycle of moving back home, getting into more debt with consolidation loans, and just paying the minimum payments. After all, I was paying my bills, so what was the harm? Then I’d branch out on my own again, struggle to make ends meet, then move home again. Mum joked I was on a piece of elastic.

The wake-up call

I met my now-husband – and father to our kids – in my mid-20s and pretty much continued living a life enslaved to debt. We weren’t struggling as such, but there were always payments to be made. After struggling for a few years with only one income between us, my husband (after years of hard graft), finally got the promotion he’d been working towards.

His salary jumped exponentially. We bought a new car. We got sofas on finance. I landed a three-month fixed-term contract and added to our income. Only, instead of paying off debt, the money got swallowed up in a spending-spree. Going from years of having next to no money, to suddenly having an extra income, meant we could go on holiday. Buy clothes. Go out for dinner. Eat lots of takeaways (and I mean, lots. I was working full time with a 6 year old and a 2 year old).

Then, right before my contract was due to end, we discovered that one of our outgoings was due to double.

Cue a strict investigation into our finances and decision to draw up a budget, pronto. I was shocked to discover that we’d been spending £1,000 a month (when we were both working full time), on NOTHING. Cash that had just dwindled away on unnecessary spending. I also had a vague idea of how much our total debt was, but it was only vague. You see the thing is, we could afford the monthly payments. So when I added up all the totals, including mobile phone credit agreements, I felt sickened to discover that the full amount of debt was around £20,000.

My progress so far

I began this journey in July 2018. Since then, I’ve brought the debt total down to nearly £15,000, by the end of May 2019. I’d love it to be more, and my goal is to have it all paid off by the end of 2020. When I first started I threw everything I had at it, and went out and got a rare part-time job that could be worked around my husband’s erratic shift pattern. That wasn’t sustainable though, as with trying to run the blog, look after the kids and house and focus on other money-making ventures, I was running myself into the ground.

Progress is steady and consistent, though. I’ve been using the debt-snowball method and it’s working well for us. I also feel extremely empowered to know that I’m in control of this. That I’ve wised-up to the banks and how they make money out of unsuspecting (and perhaps, naive) individuals. Without financial education, consumers believe that the banks are helping them out. But until you understand how money really works, you go on believing in the system and ‘the norm’ of living a life based on credit.

Once my debt is paid off, I’m going to start looking towards preparing financially for the future. I only wish I’d started years ago.

Top tips for paying off debt

Sit down and do a budget. Work out where your money is going, where you can cut back or save, and get rid of anything unnecessary (like satellite TV). Save as much money as you can to put towards your debts.

Speak to your creditors. If you’re really struggling and your outgoings are higher than your income, I’d recommend speaking to your creditors to see if you can get your monthly repayments lowered, or put on hold while you get sorted. There are also plenty of charities out there that can help you with this, such as Christians Against Poverty or stepchange.org

Take control. If you can manage to repay your debts without any third-party assistance, do so. Not only will it improve your credit score, it’s incredibly empowering knowing you are taking back the control of your own financial situation. And with so many people in the debt-free community on social media, you’ll never be alone. Debt is still very much a taboo subject, but it doesn’t have to be.

Make extra money. There are so many quick and easy options available for making extra money, from surveys and task apps via your mobile phone, to mystery shopping, to selling personal possessions online or at a car boot sale. Once you set your mind to it, you’ll be even more psyched up. You could also look at getting a part-time job (waiting tables pays tips!), or do some freelance work.

Ultimately (as with anything), the more effort you put in, the more you’ll get out. It’s entirely possible for ANYONE to get out of debt and turn their financial situation around. All it takes is commitment, support, and determination.

One Response