There is one thing that frustrates me incredibly as a self-employed person (actually there are lots of things, but for the moment!) and this is the ability to get a mortgage. It appears that getting a mortgage when you are self-employed is the holy grail of finance. Something only reserved for employed folk. And this HAS TO CHANGE.

I am going to be working with Trussle, the UK’s first online mortgage broker, over a series of posts exploring many of the issues surrounding mortgages. Trussle’s aim is to make mortgages fairer, making it easier for people to get a new mortgage or remortgage. They aim to save customers money as their service is free. And they are doing all they can to change the mortgage world by lobbying the government and banks to change their old-fashioned ways.

I quote Trussle: –

My Situation

I am in the process of selling my house and wanted to buy a new house based on my self-employed earnings. I currently live in a 4-bedroom house with an outstanding mortgage of around £200k. There are around 20 years remaining with a monthly payment of £960 per month. Very affordable. I have an existing mortgage with First Direct that I took out many years ago when I was employed, but I’m now self-employed which means the process for getting a mortgage is very different.

The Employed Mortgage Process was simple

It was a very simple process five years ago. I was earning a full-time salary of £70k with a bonus of around £10 to £15k per year. The rules varied depending on the mortgage provider, but I could generally get 4 times my salary in mortgage earnings so at least £280k.

Usually, all you need to determine your affordability of the mortgage as an employed person is proof of your income, financial commitments and outgoings – from your latest three bank statements and latest one to three payslips. A large amount of borrowing sorted.

The Self-Employed Mortgage Process is not so simple

My business works on financial years and I am currently at the end of year 4. Things are going well, my top line turnover, has got to the point of matching my final salary from my employed job.

The main difference between being a fully-employed mortgage applicant and a self-employed applicant, is that most mortgage lenders won’t look at my top line turnover. Instead they look at my bottom-line profit (plus my salary drawings) after business expenses, pension contributions and tax. An £80k turnover suddenly drops to a much lower number.

Not only this, but many mortgage lenders ask for two years’ worth of accounts and two years’ of SA302s and tax year overviews! They want to go all the way back to my accounts from September 2017 to Aug 2018. To a time when I was not making as much money and declared a much smaller profit.

Based on my circumstances, the amount I am able to borrow is too low for the kind of home I want to buy.

I’ve had a few conversations with brokers, several of whom charge a fee. And then I found Trussle, who don’t charge for their service and have been advising me on what’s possible for my own circumstances.

I am not the only one in this position

The founder and CEO of Trussle, Ishaan Malhi, found himself in a similar situation, when he left a job at an investment bank to try his hand at self-employment. This struggles he faced trying to get a mortgage, and eventually being declined, led him to founding Trussle to make home ownership more accessible.

I have countless friends struggling as well. It is frustrating as I know I can afford the mortgage payments; in fact, I have more disposable income than my employed days without a £1000 a month childcare bill to pay and expensive travel into London.

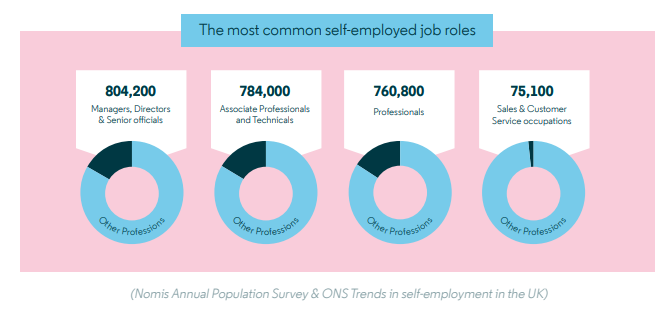

Trussle carried out some fascinating research about the UK under-served (those of us who aren’t properly served in the mortgage industry). Self-employed folk making up the biggest proportion of them. There are 4.85m self-employed individuals in the UK (based on ONS, Trends in self-employment in the UK, February 2018), set to rise to 5.5m by 2022. We are a growing part of the UK economy. 15% of the working population is made up of self-employed people.

I have noticed a large chunk of mums that I know are turning to self-employment and setting up their own businesses. The traditional working week of 9 to 5 does not fit in with childcare.

My friends are writers, cake makers, cleaners, childminders, artists, therapists, jewellery makers, virtual assistants, bookkeepers, social media managers, the list goes on and on. We are a growing community that comes from a place where the employed world will not support us in our hours and work of choice.

The latest figures prove this point – in 2001, there were 872,000 self-employed women making up 28% of the UK’s self-employed population. The latest figures show there are now 1.54 million self-employed women making up 34% of the total self-employed population.

Personal Sacrifices

Unfortunately, as it’s unlikely I’ll pass the necessary affordability tests with the lenders and qualify for the mortgage size I need, I am probably going to have to make a huge personal sacrifice and move into rented accommodation for a while.

Until I have enough profit on my historic company accounts so the lenders will consider me able to afford the size of the mortgage I need, I’ll have to rent a property big enough.

The impact of rental is going to cost me a lot. Average rent for a similar sized house in my location is around £4/500 more than my current mortgage per month. And this is potentially too much of a stretch in uncertain times.

I am also considering my location. I currently live in a very expensive location, with fast trains to London taking just 20 minutes and great schools nearby for primary and secondary. If we were to move just 20 minutes further north, still within easy reach of said good secondary school, I can buy a 4-bedroom house for £200k cheaper than in my current location. Trussle’s recent findings have shown that there’s a house price premium associated with outstanded rating schools. The additional cost of buying a home near one of the best schools is £180,000. So it’s worth considering this when looking into house prices and options available to you!

I am considering all options

And it is the same for other self-employed folk whom have made considerable sacrifices. Quoting directly from the Trussle research:

“For the most part, these sacrifices mean people’s ambitions and plans for the future have been put on hold until they’ve secured their mortgage”

For example, a third (33%) of borrowers have either delayed – or have considered delaying – their mortgage application purely due to their employment status. 7% have delayed relocating, despite their home not suiting their needs, and 4% have even considered moving back in with friends and family.

I leave you with this damning and concerning statement from Trussle. And take it from me I will be doing everything I can with my influence of my website and social media, alongside the considerable influence and efforts of Trussle to change this situation.

Trussle have some recommendations for the Mortgage Industry

- Assess most recent earnings and projections. Lenders should assess the latest year of applicants’ earnings, as well as consider building a credit risk model that accounts for future income projections. This will give a fairer and more accurate indication of the borrower’s current and future income, allowing them to borrow more. This will be especially important for any applicants whose new business experiences a growth in earnings. It should also reduce the number of self-employed applicants being viewed as economically ‘risky.’

- Consider a wider range of income streams Lenders should consider income more holistically and consider all the various income streams that a self-employed mortgage applicant may have. Financial assessments should be streamlined to ensure all income sources are accounted for, making the process fair for everyone.

- Open banking should provide easier access to financial statements automatically for the lender’s decision making.

- Suggestions for the Government HMRC have proposed a new initiative from 2020, Making Tax Digital. This initiative will overhaul tax administration, making the process more straightforward and efficient for taxpayers. This has the potential to improve the accessibility of tax documents for the self-employed, which in turn will make their mortgage applications smoother.

- With this in place, we’d encourage the Government to consider the possibilities of introducing greater flexibility in tax reporting periods, with documents being issued by HMRC quarterly. This would enable mortgage lenders to assess self-employed mortgage applicants on their latest income and tax reports and ensure they’re not being assessed on their past earnings. Much like the financial freedom Open Banking will provide, lenders should be able to liaise directly with HMRC to request customer details, provided prior permission from the applicant has been granted.

- Suggestions for the wider mortgage industry Improving communication between accountants, brokers, and lenders will ensure the specific circumstances of self-employed applicants are assessed fairly.

Trussle are doing their utmost best

Trussle are doing their best to make it as easy as possible to get a mortgage for your dream home. They are doing the following and I urge you to apply online when it’s time to re-mortgage or to get a new mortgage.

-

Helping design fairer mortgage products:

No one should miss out on owning a home due to their choice of employment. So, Trussle are using their own data to help design new products for under-served groups, like the self-employed.

-

Providing fairer mortgage advice:

Using unbiased algorithms, True Cost, and a customer-first approach, Trussle is determined to make mortgages accessible to everyone, regardless of their situation.

-

Building a fairer mortgage industry:

Trussle is working closely with lenders to identify ways to help them make faster, smarter, and more suitable decisions for borrowers, to prevent shutting anyone out who deserves a mortgage. Trussle is also pushing for more transparency through a Mortgage Switch Guarantee, making mortgage switching easier for everyone.

-

Building a fairer community:

Trussle is supporting the self-employed community through a series of workshops and ensuring there’s enough advice and support for all of those who feel under-served.

Dilpreet Bhagrath, Mortgage Expert at online mortgage broker, Trussle, has suggested the following tips for self-employed people looking to get a mortgage:

-

Be prepared with at least 2 years of documentation

Determining affordability can be a more convoluted process for the self-employed. Most lenders require at least two years of certified accounts and SA302s, proof of deposit or last mortgage statement. Plus your latest three bank statements, proof of address and identification. To avoid any issues that could delay or prevent you from getting your loan approved, make sure that your details and accounts are kept up-to-date and in order.

-

Keep your personal and professional accounts separate

Keeping separate business and personal bank accounts will help you to keep track of your spending, expenses and income, but it will also help to realign your accounts during the application process.

-

Speak to both an accountant and mortgage adviser

Many people seek advice from an accountant when considering self-employment, but it’s also worth speaking to a mortgage broker about your current mortgage or future home ownership plans. This will ensure you’re aware how to structure your accounts for both tax purposes and securing a mortgage.

-

Register for the electoral roll

Registering on the electoral roll can help increase your chances of getting a mortgage. Mortgage lenders use this to not only to confirm your identity, but also to check your credit history. If you’re not listed, some lenders might reject your application.

-

Don’t be put off trying to get a mortgage

Finding and securing a mortgage can seem like a daunting task but there is lots of free advice out there to make the process easier for you. Using a mortgage broker can be invaluable, particularly if you’re self-employed. At Trussle, we have access to over 12,000 mortgage deals so we can advise you on the right mortgage for your own personal circumstances. We assess mortgage deals on their true cost, taking into account any obligatory fees, charges or incentives so you know the overall cost of your mortgage. It’s always important to consider any personal and future circumstances when securing a mortgage and seek advice to ensure you’re aware of the options.

This is a collaborative post with Trussle. You can read a complete version of their Mortgage Saver Review here.