And why you should think carefully about using this product.

I recently bought a bed and mattress from Wayfair in their sale. I needed a bed, I did not want a bed. My three boys have moved from one shared bedroom to a bedroom each, my 12-year-old needed a double bed and desk. As I was checking out, I saw the priority option to pay using Klarna, which is a buy now, pay later scheme. I could have the bed now and pay back the £176 in three instalments interest free. Wow, free stuff that I can spread out the cost on.

Clothes Purchases

I do not have an ASOS account, I prefer to buy clothes in the shop and try everything on. In the name of research for this article, I opened an account last week and ordered a pretty summer dress.

This was the first screen; Klarna and Clearpay are both mentioned as payment options. It’s almost like they want you to pay using Klarna. Strange that.

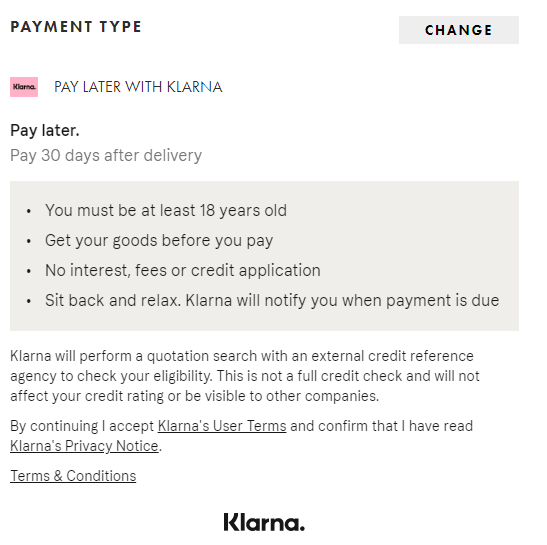

The payment process continues and the emphasis on Klarna is lower, but there are two payment options, pay later with Klarna (in 30 days) or Pay in 3 with Klarna (3 monthly instalments).

Here is the description from the website. You must be 18. Great I should think so too. Get your goods now (woo hoo for free!), no fees or interest great. And then ‘Sit back and relax’, really?? What about save up the money and ensure that you can AFFORD to pay for your goods when your payment is due. Maybe some warnings about the adverse effect on your credit file if you cannot make the payment in 30 days’ time? Maybe a note to say, if you can afford to buy the clothes now, just buy them using your debit card, do not choose the pay later option and forget.

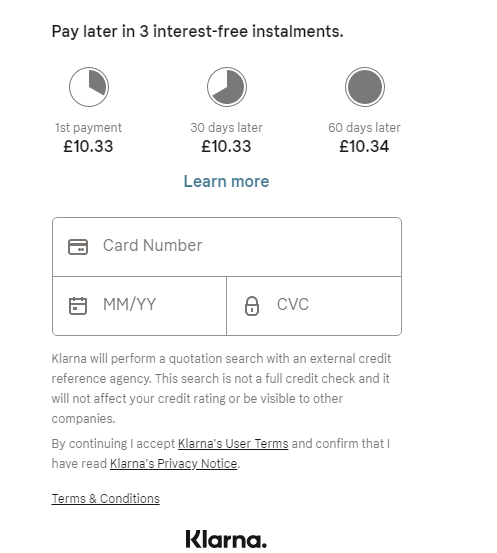

This is the information page if you click on 3 interest-free instalments.

And then this. The marketing slogan on the home page of the Klarna website. Which makes me angry.

Klarna – effortless, safe, and fun? Fun? Really? When has getting into debt ever been fun? Klarna is a debt product. You are borrowing money from Klarna to get your clothes, or trainers or furniture now and paying for it later.

And what happens in 30 days’ time when you cannot afford the repayments?

I spoke to a friend’s son who recently got into debt trouble with dire consequences.

Robert (a made-up name to protect his identity) is an intelligent 18-year-old young man. With a mind beyond his years. We talked about his intended career, his current caring job and its stresses, his new dog. I told him about my job, and he shared his recent and still raw debt story with me.

He was able to access £2,000 of credit from various debt providers, including Klarna. An 18-year-old with a low credit score, of around 250, yet he was able to get £150 of clothes and take the 30-day payment plan with Klarna. He took out two credit cards with high street banks and got another £700 of credit from them, and then Nationwide gave him a £1,000 personal loan.

Firstly, I am shocked an 18-year-old with this credit rating was able to get this many products in close succession. The checks obviously were not monitoring that he had applied for several credit products in the same time period.

He soon found himself in £2,000 of debt, and after 30 days, had no way of paying the £150 Klarna debt or the payments on the credit cards and loans.

Desperate Times

It overwhelmed him, he felt helpless and one night he drank too much and swallowed a bottle of pills.

Thank the lord he went straight home to his parents in a stupor and they worked out what he had done, rushed him to hospital to get his stomach pumped. The following day he opened up and told them of his debt and his feelings of helplessness.

They paid off his debt and put him on a monthly payment plan of £100 a month to repay to them rather than the debt companies.

What I Object to

I hugely disagree with the marketing behind the Klarna buy now pay later product. The world (and the Instagram world) is a hugely commercial and materialistic world. We see things on Instagram, we see our favourite people loving products and want them for ourselves. This is just society, and this is not going to change for a long time.

But then Klarna comes along and says Oohhh, Lynn, you can have that jumpsuit you want right now, and you don’t need to pay for it for 30 days, or you can spread the payments over 3 months. I then might think brilliant, free stuff. And then I get a pair of trainers using Klarna or Clearpay. And then I get my bed using Klarna, and then I get some school shoes for the boys using Clearpay. It all adds up and becomes a complex mess of so much money spent that must be paid back at various confusing times.

If I do not pay it back, there will be nasty repercussions for my credit file. Non-payments or defaults will be marked on my file, and this will stay on my credit file for six years! This could affect much-needed credit applications for a mortgage, a car loan, or a mobile phone.

Klarna and every retailer who now using Klarna as a payment option need to make it crystal clear to their customers what they are getting themselves into. And the consequences if repayments cannot be made.

A Credit Card

I do not object to credit and personally use credit cards and loans, provided I can afford the monthly repayments. I have a credit card that I pay off in full each month. I use them for the purchase protection they provide and to get an annual cash back bonus reward.

My first experience of debt was at age 18, and then I spent the next 24 years in various levels of debt. I have had every credit card you could imagine, personal loans, store cards, and buy now pay later deals. Finally, in 2019, I pulled myself out of debt after paying off £16k of credit card debt.

Fortunately, I have always been able to at least make the minimum repayments but believe me I have felt the desperation and stress of endless debt payments and the feelings that I will never be out of debt.

I feel like I learnt it was socially acceptable to be in debt, particularly as that vulnerable 18-year-old. I’d just started university and having that Barclays credit card and overdrafts thrown at me, all that ‘FREE money’. Then I hit Top Shop, Dorothy Perkins and Miss Selfridge and bought clothes on a store card, ‘FREE clothes’.

The same cycle is repeating now, but it feels worse. Klarna and other buy now, pay later firms feel predatory, normalising debt.

Save up and Use your savings

Very simply put, save up and buy using your savings. Wait a month, or a year, or five years, and save up for that thing you need. Establish if it is a need or a want. I would love a new Prada handbag so much. But do I need it? Absolutely not.

What do you do if your debt is worrying you and you cannot afford the repayments?

The first thing to do is get a handle of what debt you have, with which companies. How much do you owe, when are payments due, how long does the debt last for and what is the interest rate?

Call the companies that you cannot pay and tell them. I spoke to Klarna at length to share my concerns about their product and misleading marketing and they did say that anybody in trouble must call them and they will help the person. Payments can be delayed; interest may be frozen. But the money still must be repaid at some point. There is no magic money fairy that takes the debt away. You buy now, you pay later, and there’s no escaping it.

If you are feeling totally overwhelmed reach out to a wonderful debt charity for help. Step Change, Citizens Advice Bureau , Christians Against Poverty are all incredible charities that will help you out FOR FREE. They will help you to budget and work out a plan to repay the money in a way that is right for you.

I have so much debt-related content that can all be found in this specific debt section. From debt stories from many money writers, to my story and specifics that will clearly help you to get some control and guidance.

Or reach out to a friend, chose a friend who you know is sensible with money and will not judge you. They can help you to come up with a plan to attack the debt and get it repaid.

Disclaimer. I did speak to Klarna at length about this story who offered to help the person I mentioned, but he did not want their help.

4 Responses

Great article. The ‘always interest free’ is misleading no? The 3 instalment plan in your example seems to add nearly £1 to the price

I struggle to understand how Klarna get away with this advertising.

Getting into debt is not fun. It’s bondage, scary and filled with worry, stress and anxiety.

I had a friend who came here as a international student. She came across Klarna and quite literally thought it was free money. Purchased goods and forgot about it . But it didn’t forget about her! She soon got a shock. Luckily she was able to pay it back .

But some can’t.

Debt is not normal. If you don’t have the money – sorry you cant buy right now.

Emphasis should be on how to afford things. A new job? Overtime? Side hustle? This lazy mindset needs to be abondoned.

Great post!

Thank you so much for a brilliant, helpful article. Like so many others I have experience of credit card debt which took years to pay off. The more folk understand that companies offering credit without due care and attention really are not their friends, the better, and your piece make this very clear.

(It’s also worth pointing out that very often, with things you want, but don’t really need, the novelty and thrill of ownership wears off very quickly and you wonder ‘what was that all about?’ Things like that aren’t worth getting into debt for.)

thanks