The thing that I find very frustrating about the financial world is the amount of terminology used to seemingly confuse people into thinking that it’s complex, when it really isn’t. It is one of my business and life missions to talk simply about these complex matters, so EVERYONE realises that personal finance is simple. With this article I am going back to basics and have created a pension terminology buster.

I have picked out the commonly used terms or abbreviations and have explained them in simple real language. This will be a useful tool that will help you to understand the world of pension terminology and you will feel comfortable with this important area of personal finance.

A huge thank you to Eve Keith, a Pensions Manager and expert of 20 years in the industry for helping with article.

Pension Basics

State – Workplace – Self-Invested

State Pension

The state pension is built from contributions to national insurance (NI). It becomes payable later in life. This age can change based on government decisions and is expected to change in the future. For the latest retirement age for men and women visit the government pension website

You must contribute NI contributions for 35 years to be eligible for the full state pension. Again, you can check your NI contributions on the government website. This is key for women to check as you may have gaps when you have had years out of work. Another inconsistency for women is that during maternity/childcare leave years where you may have a significant NI gap. Check your own record and have the knowledge. Check if you are eligible for NI credits, for example for a period where you are on Working Tax Credit, Universal Credit or Carer’s Allowance. If you reach retirement age with, say 25 years of the 35 in NI contributions your state pension payment will be reduced. This can be topped up by you or your partner at any time before retirement.

It is very unlikely that the state pension will be enough for you to survive on, the government is even saying this. It is advisable that you start paying extra into a pension, whether a workplace pension or a private pension from as early as possible.

Workplace Pension and Auto-enrolment

If you are employed, pensions are a no brainer. Your employer is giving you FREE money. For every chunk of salary that you pay into your pension, your employer will be doing the same. Every employer is different, but they must at least put in 2% for every 4% that you save. The pension contribution is taken from your pre-tax earnings and is an auto-enrolment, (subject to lower earning thresholds). Auto-enrolment is where employers sign employees up for a workplace pension unless the employee chooses to opt out. It is FREE money, why would you opt out?

Your employed pension is accessible at a younger age than the state pension, currently from age 55 at the earliest, changing to 57 from 2028. Again, this age can change with government policies so it’s best to check with your work pensions provider. Most likely though is that if we are still working in our 50’s, it is sensible to leave the pension money until you definitely need it for living expenses.

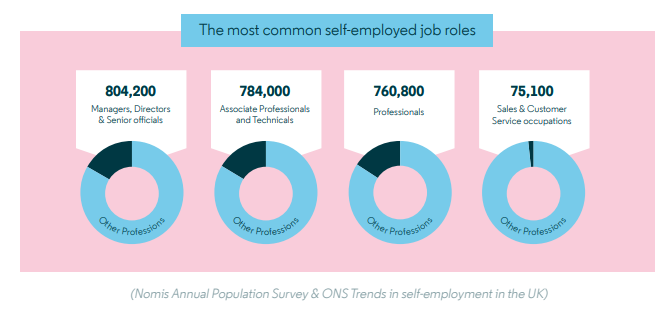

Self-employment and Pensions

Inevitably, pensions are trickier as a self-employed person. But setting up a good pension scheme that works for you is totally doable. Maybe you are like me and have a few pension pots dotted around from previous employers, you can consolidate then with PensionBee and then add to it as and when you choose. Or you can set up a regular transfer. It totally depends on how regular your income is. Mine is very sporadic, so when I have a good month, I put money into my pension, when it’s not a good month, I don’t.

The great thing about pension is that you get tax relief. If you are self-employed, you can include your pension payments on your tax return. And if you are a higher rate taxpayer, it will reduce your tax bill, you will need to include it as an expense in your tax return to reduce your tax bill. Or if you own a limited company your company can contribute into your pension for you, reducing your corporation tax payable. If you are a higher rate tax band payer this is well worth doing!

Other Types of Pension

Of course, you do not have to have a private pension. Many finance experts suggest different ways to manage your money. You can invest in property or stocks and shares ISAs as an alternative. I would always suggest a balanced approach is good – it makes sense not to put all your eggs in one basket. Spreading your money around several different options to diversify your risk and return reduces the likelihood of you being held at the mercy of, say, a state pensions crisis or a massive financial markets crash.

Overall, pensions are a very tax efficient way of saving, as either the money is deducted from your earnings before tax is taken off, or your pension company adds the tax relief. The money is locked away for, potentially, a long time but it’s totally worth it – if the worst should happen to you before you draw on your pension, you can name your loved ones on the policy ensuring they can benefit.

Pension Terminology Defined

Private Pension

This is a private pension plan that you can set up and save into as an individual. If you don’t have a workplace pension to pay money into or are self-employed, then this is your pension option. There are many pension providers out there with simple fund choices. Be sure to investigate company with low fees, with a choice of pension funds that you are happy with and that has great customer service.

There is also a SIPP option Self Invested Private Pension where you are responsible for your investment decisions.

DC Defined Contribution (often known as a Money Purchase Scheme)

Many modern pensions are defined contribution. All my employer pension schemes that I paid into from 2000 until 2015 were defined contributions. The private pension scheme that I pay into now as a self-employed person is a DC pot. This is where you or/and your employer pay into a pot of money.

You can have various pots of DC pension contributions which can be complex to keep track of. It might make sense to combine these into the same place, annual fees and transfer fees dependant.

DB Defined Benefit (often known as a Final Salary Scheme)

This was a type of pension offered by some companies in recent years, it has become rarer as it’s a lucrative employee benefit. I was never lucky enough to be offered this during my employed life. This gives you a guaranteed income every year from your retirement. It pays you an income based on your salary (it could be average or final) and the number of years you have worked for your employer.

This type of pension is managed by the company you worked for and should never be transferred without advice from a qualified and recommended financial advisor.

AVC Additional Voluntary Contribution

These are additional payments that you might want to add to your pension pot. Maybe you want to save more than your current employment contributions. Check with your HR department, as if you contribute more sometime your employer might match some of those contributions.

You may also want to make additional contributions for tax reasons to stay beneath a higher rate tax banding or for child benefit reasons (this benefit is tapered after a parent earns £50k or stops after a parent earns £60k)

Drawdown

Pension drawdown is a way of getting an income from your pension whilst allowing your pension fund to remain invested and to remain growing. This is only applicable to DC pension pots.

Annuity

You can use your pension pot money to buy an annuity policy. This gives you an annual income to be paid to you for the remainder of your life. Up to 25% of your pension pot can be taken tax free at retirement age. You can choose to buy an annuity with the remainder.

Enhanced Annuity

Pension providers may offer an enhanced annuity where you have a medical condition, or are a smoker, which the provider feels may lead to a shorter life expectancy. Not all annuity providers offer enhanced annuities, so you should check as many providers as possible if you think this may be relevant to you.

Cash Equivalent Transfer Value (CETV)

A CETV is the cash value placed on your pension benefits. This is the amount that would be paid if you elected to transfer to another pension arrangement.

Life-time allowance

This isn’t a thing that affects too many people! There is a maximum amount that can be saved into a pension. The government have reduced the limit over the past few years from £1.8m to £1,073,100 in 2021.

Annual Allowance

There is a maximum amount of pension savings that can be made in a tax year which benefit from tax relief. For many people this is £40,000 per year however for some a different threshold applies so do check yours.

Deferred Pension

Pension savings are accessible at different ages depending on the types. If you chose to leave it later to access this money the higher your potential pension pot and income could be.

ESG – Environmental, Social and Governance

This is the term that refers to a set of standards by which you choose to invest. Environmental refers to the green policies of a company, carbon footprint, recycling, plastic usage. Social refers to a company’s relationship with staff, customers and communities. Governance is a company’s leadership, internal controls and shareholder rights.

You can choose to invest in your pension in an ESG manner that reflects your own personal morals and beliefs. Contact your workplace pension department to find out how your money is invested or put your private pension money into a plan that matters to you.

I choose to invest in an environmentally friendly pension scheme. The fossil fuel free fund with PensionBee. This pension plan excludes fossil fuel producers, tobacco companies, manufacturers of controversial weapons and persistent violators of the UN Global Compact.

Pension Protection Fund

The Pension Protection Fund (www. https://www.ppf.co.uk/ ) was established to protect people with a defined benefit pension when an employer becomes insolvent.

Pensions Wise

If you are still baffled and need help to understand your pension visit Pension Wise for free advice. This is only available to over 50s (and isn’t right and needs to change). You can book an appointment to explore your pension options.

The Pensions Advisory Service

Members and beneficiaries of occupational pension schemes who have problems about their scheme which are not satisfied by the information or explanation given by the administrators, or the Trustee can consult The Pensions Advisory Service (TPAS) (www.pensionsadvisoryservice.org.uk). A local TPAS advisor can usually be contacted through a Citizen’s Advice Bureau.

Summary

The pension world is complex but this article defines all the scary pensions terminology terms. Take control of your pension. Understand how much you have and how much is enough to save and get you through that period of your life when you no longer want/have to earn money.

Risk warning

As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice. This post was written in collaboration with PensionBee.

3 Responses

I was just looking into my pensions and stumbled across this article. Very comprehensive and answered all of my questions! Thanks for sharing, Lynn.

Hi Lynn

Really great article covering the terminology of pensions. I just wish that saving for retirement was made simpler and easier for people to understand. The industry loves acronyms such as LTA, ESG and VPS.