How does financial planning work? [ad]

A question that has crossed my mind many times in the past few years, since I have taken my finances more seriously, is how much money do I need for the rest of my life? It felt like a huge unknown. Have I set enough aside? Am I currently putting enough money into investments and pensions? It was all a bit of an unknown until I had a session with a financial planner from Drewberry.

What is a financial planner?

A financial planner does things differently to the traditionally more well know financial advisor. They take a holistic look at your entire life to see how much money you need for the rest of your life. They look at the income side of what you have now, what you will have in the future in terms of earnings and what you are putting aside. Spending is also an important factor and how that changes over time.

The answers you get are based on many different scenarios so you can see the impact of different financial situations and how long the money will last based on each scenario. Fascinating stuff!

My financial planning session

I really enjoyed my planning session, which felt a bit like a counselling session! Sam, my financial planner, asked lots of introspective questions about my lifestyle choices and thoughts for the future. We spoke on the phone for the first information gathering session.

Retirement Age and Lifestyle

It was particularly interesting to think about what age I intend to retire. I don’t like the word retire as it feels like a finality of life, that you stop working and its all over. I prefer to think of an age when I want to be financially independent by, to have enough money set aside to not have to worry about earning to pay the bills.

What I also take into consideration with this decision is what I do for a living. You see I love my job, sometimes it doesn’t feel like a job because I enjoy it so much. What I do every day, writing, speaking, inspiring others is the most amazing job with the added extra that I get paid to do it.

And I see it carrying on like this for the longer term. I see my business continuing to grow and grow and it being particularly important to ensure that I am staying ahead of the blogging/influencer game.

What are the current risks?

Do I think there is a risk that it could suddenly end? In short no. It is an industry that I have thrown myself into for more than six years and have worked incredibly hard to get to the top. And I will continue to work hard to stay there. Absolutely this is something that will see me through to financial independence and beyond, as I don’t intend to stop as soon, I have ‘enough’ money for the rest of my life.

For the sake of the modelling, we chose the age of 65 for an age to start drawing on my pot of money and when I will stop earning.

We also discussed life and expenses on retirement. I would love to spend lots of time travelling so this extra budget requirement was added in on top of standard living expenses.

Attitude to Risk

We talked about my attitude to risk and went through a short questionnaire. No surprise to me was that I am risk taker (I did give up my well-paid corporate job to set up Mrs Mummypenny!). When it comes to investments, I am happy to put my money into greater risk funds that may provide a higher return but there also a great risk of losing money.

Expenses

We discussed any big expenses coming up over the years before financial independence. The main one I am currently putting money aside for is the boy’s decisions at 18, and if they want to go to university. I will have some money set aside for them which will cover the money they need on top tuition fees and maintenance loans.

And if they don’t choose university, they will have a pot of money for a deposit on a house or to go travelling. It is all in my name so I will have some say over where that money goes!

My current investments and how I plan to contribute to them

We talked about my current investments and how I plan to add to them over the year. My main investment is my PensionBee pension, currently worth £50k, and I intend to add £6k per year to this fund. We also talked about the growth plans of my business and how much spare cash I would have to invest extra money.

Sam went away with all this information and plugged it into a financial modelling tool. A week later we arranged a second call and went through the results using screen sharing. There were lots of different scenarios that we looked at, but I have pulled out the three key scenarios that stood out for me.

Scenario 1 – Base Model

The information is presented back with a focus on this graphical format, with information on my current assets, my intentions to put money into my savings, investments and pension. And then drawings on my money from a retirement age set at 65. It is also based on a higher risk strategy for my investment. And average market conditions. I was pleased to see a positive looking graph.

The part to focus on is the section after retirement when the blue turns to retirement orange. This is where the blue lines of income stop, and I would start to draw from my retirement assets. I can continue drawing from my assets until I die. If the amber turns red, you have a problem and the money has run out.

This was also reassuring in that my expected income for the foreseeable future is considerably higher than my total needs, so I can clearly put more money aside into pensions and investments during my immediate future years of earning.

Scenario 2 – Moving investment to a less risky place from retirement

Higher risk can be taken when you know that your money is locked away for many years to come, and it is recommended that investments and pensions are moved to less risky funds when the time comes to draw on the money. In this example my money is moved into less risky funds with smaller returns at the point of retirement.

We see a difference here immediately; my money runs out later in retirement.

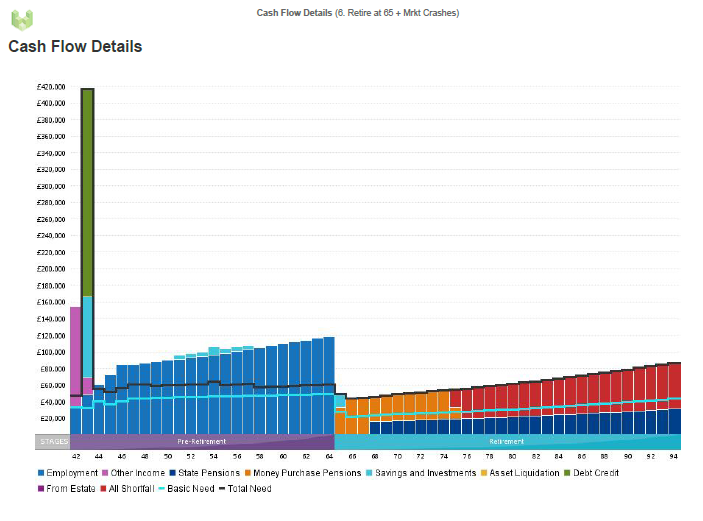

Scenario 3 A more prudent view is to look at the impact of market crashes.

A very scary view that if there were market crashes, on average happening every 10 years, then my money would run out in my mid-70s.

Learnings for me

I need to be more prepared for a prudent financial world and to put aside more money that I am doing currently.

My current £500 monthly pension contribution gets me to a total pension pot of roughly £600k by the age of 65. But I can make a significant difference to this by adding more pension contributions particularly now when my income continues to grow and there is such a gap between earning and required expenses.

The overriding feeling is that I feel reassured that my current contributions are most likely enough for financial independence by my mid-60s. Considering I had an over-riding feeling of worry until this point, that I would not have enough money, this is a huge positive!

Are you Interested in having a review for yourself?

You can book a full financial review with Drewberry. The initial review to assess suitability will be free and then if you have a full review using their advisors and financial planning software there is a fee of £1,000. Check out this video from Drewberry giving information on their approach to financial planning.

This is a collaborative post with Drewberry.

2 Responses

thanks

Navigating through the Warlito Tools platform is incredibly simple, making it accessible even for beginners. You can easily browse through different categories, select your desired modification, and apply it with just a single tap. The app is lightweight and doesn’t consume much storage, ensuring it runs efficiently on most Android smartphones without causing any issues.