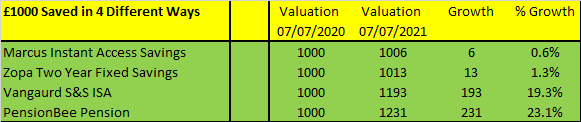

In July of 2020 I decided to try out the ultimate savings experiment. I have £1000 saved in four different ways and am tracking the growth over time, and this is my one-year update.

I have £1000 saved in four different ways or savings places, from immediate access cash all the way through to my pension. The first savings place is a Marcus Instant Access Saving Account. The second place is a fixed term cash savings account from Zopa. The third place is in a Life Strategy 80% equity fund, Stock and Shares ISA with Vanguard. The fourth place is in my PensionBee pension, it was in the Tracker fund until the end of 2020 and was then moved over to the Fossil Fuel Free fund.

How have these four different methods of savings performed over time and where is the best place for my money?

Immediate Access Cash Savings

I keep my emergency cash savings (and my tax money) in my Marcus instant access savings account. At the time of opening, early 2020 it was the highest interest paying instant access account. But a lot has changed over the past year, with regular emails received to say the interest rate was dropping.

My £1000 Marcus balance over the past one year has earned just £6.23 interest, an average rate of 0.62%.

Saving in cash is never going to give you much of a return with current interest rates so low and looking to stay low. But it is the right place to put emergency and very short-term savings. The money will only ever go up in value with the teeny interest rate, its risk free and I can access the money immediately.

Fixed Term Savings Account

My next method of savings choice was to open a fixed rate ISA savings account with Zopa Bank. I put £1000 into this account, which was brand new product from Zopa at the time with a market leading interest rate of 1.3%.

This is a fixed term account meaning that I cannot access my cash for a two-year period, in return I receive a more favourable rate of interest than an instant access cash account.

My £1000 Zopa fixed term savings, over the past one year has earned £13 interest, an average rate of 1.3%.

Again, not a great amount of interest, although if I had locked away £10k, that would be a £130 return. Fixed Term Savings accounts are a good option if you know you won’t need the money for a one-year, two-year or even five-year period. It is risk free with your return being guaranteed.

Stocks & Shares ISA

My third choice of savings is my Stocks & Shares (S&S) ISA with Vanguard. A S&S ISA is an investment product, not cash, meaning that it comes with risk. Within my S&S ISA I invest in a fund (a balanced mixture of company shares 80% and bonds 20%) and benefit from the gains if that fund increases in value or make a loss if that fund reduces in value.

Investing is a medium-term savings product, where you should leave the money for at least five years. This way you would hope to ride the ups and downs of the stock market. Be aware that your investment can go up as well as down.

The money is accessible within a few days if you need it and to access your cash you will need to sell your investment. It is not suitable for emergency money, as you might need that money when markets are down, and you may have lost money on your original investment.

As standard I put £100 per month into my Vanguard S&S ISA. This saving taken from the monthly income I draw from my business, this money goes into a 100% Equity/Shares Life Strategy Fund.

I put my £1000 savings in July 2020 into an 80% Equity Life Strategy Fund, for simplicity this means I can track the performance of my £1000 separately for this comparison.

I am SUPER happy with this performance. Of course, it has been a strange year for investment and there is an element of good timing with the markets here. I bought when the markets were low, now worth considerably more. I would say this is an unusual return for a one-year period, unlikely to be matched again.

This does highlight the huge different between cash saving and investing. Cash has paid at best 1% over the last year when investing has given this significant return of 19%.

My PensionBee Pension

The fourth choice of savings was to put £1000 into my pension with PensionBee. My pension is a very long-term savings pot that I am unable to access until the age of 57 (this age increases from 55 to 57 from 2028, but the age might change again depending on government rule changes). This money is my intended income for when I no longer want to, or must, work.

Pension money again like the S&S ISA is invested into a fund of my choice within the PensionBee range of plans. Initially my pension was invested in a standard low fee tracker fund, but I moved this over to the Fossil Fuel Free fund when it was launched in January 2021 for personal ethical reasons. I have taken this change of fund into account with my growth calculations.

My £1000 saved into my PensionBee Pension has grown by £231 in one year. The valuation at July 2021 being £1,231, a growth of 23%.

What an incredible growth over the one-year period. Again, for reasons as mentioned with the S&S ISA, timing in the market has helped here. I don’t expect many or any more years like this one, but my pension has grown very nicely. I am also happy to share that I have been contributing £1000 a month to my pension over the past year as well. My pension pot is looking very healthy after a year of growth via contributions and gains.

Add to this growth the tax benefits of pension contributions. I contribute via my limited company, an allowable expense saving me 19% corporation tax. As a self-employed or employed person you’ll usually qualify for tax relief at source. Which means that if you add £80 into your pension, HMRC will add in another £20 in tax relief, all done via PensionBee.

Summary of Results

Its blatantly obvious from these numbers that the growth in investing via S&S ISA and pensions is significantly higher than the growth in cash, I really didn’t expect it to be this different!

I will continue to limit just my emergency money (and tax money) to be held in my cash savings with all other savings going into my pension and S&S ISA (with more emphasis on pension contributions whilst in my current aggressive build stage).

Please be aware that any form of investment can go up and down. You may want to consider advice from a qualified IFA. Just make sure they come recommended by a trusted friend and check their investment levels. Some will only work with clients with an investment level of at least £150k. This post was written in collaboration with PensionBee. Capital at Risk.