The employment landscape is changing, and more and more people are making the decision to go freelance, become self-employed or set up companies.

I am one of them. In 2015 after I set up Mrs Mummypenny Ltd, after working in the employed world for 16 years. Being your own boss is the best. You are running your business, making your own decisions every day, controlling your own destiny. The most important thing for me was flexibility, being there for school drop off and collection, school events. I love being able to work the hours I choose. If I want to work 18 hours one day or two hours the next, that is fine.

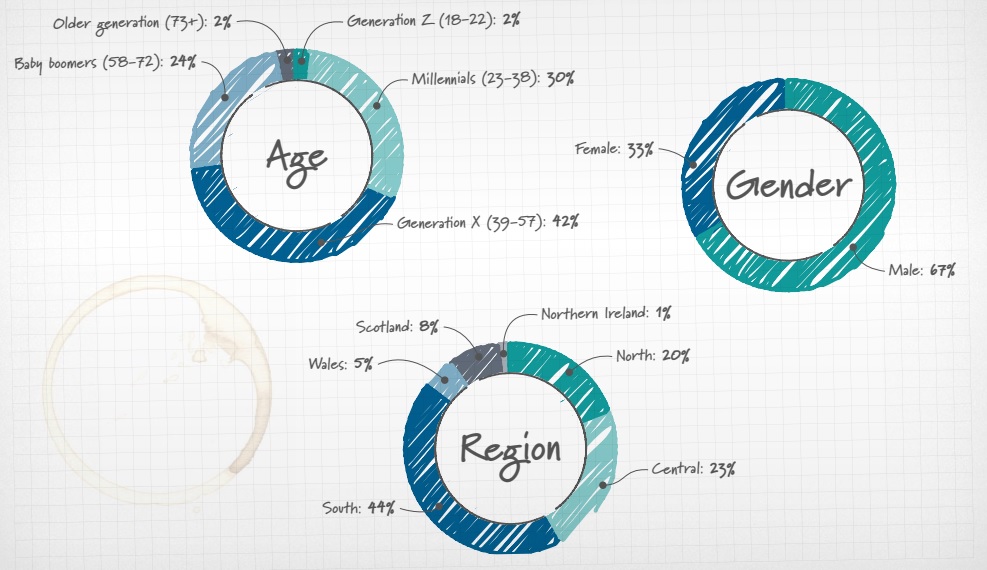

Fidelity’s recent research* found this. A significant 30% of the people surveyed as a millennial (aged 23 to 38) were self-employed and 42% of Generation x (me! aged 39 to 57).

But there are lots of things about running your own business that require consideration and action. And many things that if you get wrong, can cause the business to fail and for you to lose money. If you are thinking about going self-employed then you need to consider these things.

Getting Advice

Before starting and during your business life you must spend some time planning. Get advice from others who have started similar businesses. People will surprise you, if you ask for help, you will normally receive it. I received help from so many people in the early days of Mrs Mummypenny. So many gave up their valuable time to offer guidance on growth plans, legal structures, cost control and income generation.

As your business grows and develops reach out to those with expertise in the areas where you need help. I am currently working with a marketing expert helping with my long-term strategy and an agent to help with negotiation of multiple deals. I realise that I cannot do everything and am calling in the experts to help with business areas that I am struggling with.

When starting a business ensure that you write a business plan (Virgin Start-Up has a good one) which is going to make you think about income, expenses, risks and opportunities. You can get help and guidance from free business advice services. In Hertfordshire we have Wenta, government funded small business training and advice. I have a free business advisor and can attend many free courses from social media to back book-keeping to help with the early days of finding out everything.

Doing your accounts and taxes

You must keep good records of your finances for your business from day 1. Set up a separate business bank account and flow everything you receive or spend through that account. My business bank is Starling and highly recommend their app based FREE banking.

I would also recommend using a booking keeping software as well, Freeagent is great, it syncs with your business bank account.

I am a qualified accountant, but I employed an accountant from day 1 of running my business. It was important to have someone else produce my accounts and take the ownership and responsibility away from me. He ensures that my limited company accounts are submitted on time and my tax bill is calculated correctly.

This is a mega important thing to get right, whether you are a sole trader or limited company, you must submit correct accounts to HMRC and pay your tax.

Cash Flow Management

This is the part of self-employed life that I have struggled with. Very simply put your income must exceed your expenses and your salary that you draw from the business on a monthly basis.

The summer of 2017 and 2018 were tough months for income generation and business expenses and I didn’t keep a close enough eye on my cash flow management. I had to borrow money to get myself out of the cash flow issue.

A cash flow forecast model is an important one to do. And it doesn’t have to be complicated. In a spreadsheet look forward for a year and for every month include your expected income and expenses. And don’t forget to include your personal drawing from the business, in fact use a pay yourself first model.

This will give you a month by month view of when you are tighter cash flow wise and you can plan accordingly. This is the most common reason for businesses failing.

Putting Money Aside

Following on from cash flow it is important to put money aside for a few things.

Emergency Fund

Firstly, as with the personal finance world, you should put business money aside for emergencies. It can used for unexpected big business expenses or cash flow issues. I would recommend building this up to at least three months of business expenses.

Tax and National Insurance Account

You will need to set aside money for your tax and National Insurance contributions. Speak to your accountant to get an estimate of what this payment will be based on expected income less expenses. I set aside 20% of my turnover into my tax account.

Savings into a pension fund

The biggest difference between self-employment and employed work is the pensions contributions. No longer can you contribute to a pension with a nice free contribution from your employer as well. And when self-employed no one if forcing you to put money into a pension, as in auto-enrolment.

I cannot stress how important it is to set up a pension and to set money aside for retirement. The current state pension is far from enough to live on after retirement. If you want a comfortable life with spare money for fun, then you need to save money into a pension fund.

Its never too later to start. And the best time to start putting money into your private pension is now. Fidelity have done a huge piece of research* that be accessed here. They have found out the following

- 62% of self-employed people have no pensions savings

- 39% of self-employed people have never even heard of a SIPP (self-invested private pension)

- The most popular way of saving for self-employed people is an ISA 39%.

- 61% of self-employed women do not think that are saving enough for their future.

- 25% of self-employed women worry that that would not be able to afford a maternity leave.

The fidelity reports gives lots of simple and reassuring information about savings and pensions and is well worth reading.

I recommenced my pensions contributions three years after becoming self-employed. I had to wait for income stability before locking that money away for the next at least 13 years. The aim is a £500k pension pot which should be enough for retirement. My current pot of £50k will generate around £30 of income a week. This is nowhere near what I will need.

This is a collaborative post with Fidelity International.

*research is based on a survey of 1032 employed people and 1028 self-employed people in January 2019 by Comres for Fidelity International

One Response

Before starting your own business, I advise you to research the market and study the needs of consumers. During the pandemic, dietary supplements have become more relevant than ever. Now you can successfully grow sales on Amazon even if you don’t have actual production by partnering with vitamin manufacturer