A question I often ask in conversation with friends is ‘Where do you keep your cash’. I know, a taboo subject to talk about, but I love talking about money! I am intrigued to understand where people keep their money and their attitudes to risk with that that money. Mostly I talk to my girlfriends about this over dinner and I hate to hear it, but mostly their money is held in cash. They have savings accounts or cash ISAs with a good amount of money in there earning my friends very little interest and a tiny return.

Why do so many leave their savings in cash?

But why? Why are so many of my friends, intelligent, educated women holding their savings in cash?

The Emergency Fund

First things first. It is sensible and advisable to have an emergency fund that is in cash that is easily accessible. The amount in here should be enough to cover your monthly outgoings for around three-six months. Whatever you are comfortable with.

Personally, I am good with around three months of cash savings. This emergency fund should only be used for, yes you have guessed it, emergencies. Things like the boiler needing replacing or a new washing machine. Or if the worst happened and you lost your income, you would have the bills paid for a period of time. If an emergency happens and some money is spent, it must be replaced as quickly as possible ahead of putting money elsewhere.

Repayment of Interest Accruing Debt

Secondly, the other thing to mention is that one should think twice about investing if you have that has high interest accruing. Payment of credit cards or loans with higher interest rates should be prioritised first. This doesn’t apply to your mortgage which is most likely at a very low interest rate. Again, with personal experience I have some debt being paid off currently, all at 0% interest, so I am quite comfortable paying off that debt at the same time as investing money into stocks and shares.

Excess money can go into Investment

For any money in excess of this emergency fund, I personally move money into investments. I am not happy with the amount of return I get on cash savings and feel comfortable putting my money into an investment wrapper which could give a better return on my money. I personally choose the tax-free stocks and shares wrapper for my investment perfect for beginner investors and sophisticated investors alike.

The money that goes into my ISA is being saved for long terms goals five to ten years down the line. I have chosen a slightly higher risk portfolio with potentially higher returns, and potentially higher losses. I fully understand that with the potential risk of making money I can also lose money.

Attitudes to Risk effect your views on Investment

I believe it comes down to your attitude to risk. I asked one friend recently what scares her about investing in stocks and shares. Her reply ‘The value of investments can go down as well as up’. So the fear of losing money far outweighs the opportunity of potential gain. She feels far more comfortable watching her money slowly grow in value terms. However in reality she is actually losing money after inflation. She is most likely only earning around 1% on her cash ISA with inflation at around 2.5%. Meaning a loss in real terms.

It is interesting to recognise that some people are simply too uncomfortable with the potential downside of investment loss. I do not share this view. I have been investing in stocks and shares for my entire working adult life and have benefitted greatly from returns I have received. Having seen this in action and pocketing the profits I am more than comfortable with the risk.

I know that my money is locked away in its investment pot for a long time, so I am more than prepared to take the risk and ride out any downs (its down currently due to current market volatility) and ups and benefit from potential returns in years to come.

Are you considering investing your money? Why not consider Vanguard?

I am not confident enough in my knowledge of investment to decide on individual stocks (and have been burnt in the past with some share dealing losses) so I would rather put my trust into a well-established company, with a proven track record. A perfect place for a beginner investor to start is with a stocks and shares ISA with Vanguard.

Vanguard are a well-established investment company trading since 1975. They have a brilliantly simple beginners guide to investing that makes the choice of where to invest ever so simple.

Once you have chosen your type of investment account (ISA, Junior ISA or General Investment Account) you choose your fund. The LifeStrategy fund range is a great option to look at as there are five funds to suit different risk appetites. LifeStrategy 20% Equity has a low amount invested in shares so is relatively low risk, compared to the higher risk LifeStrategy 100% Equity fund which is fully invested in shares and is much higher risk. The other three funds in the range sit between these two with a more moderate amount of risk. The reason I like these funds is that they hold investments from all around the world and are very low cost.

Least Risk to most Risk LifeStrategy Funds

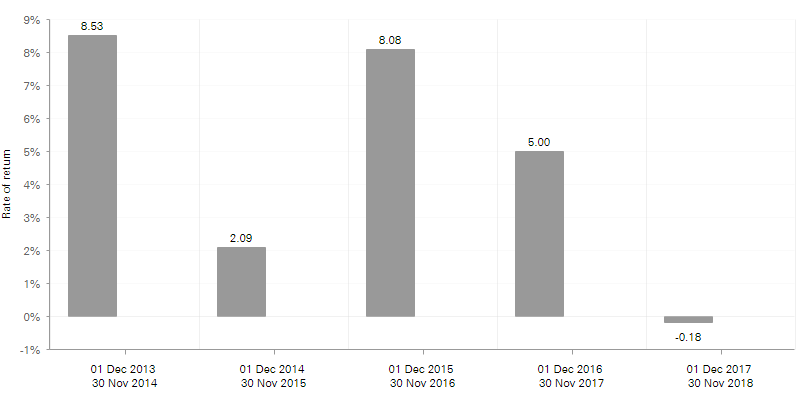

The LifeStrategy 20% Equity fund is the least risky fund at level 3/7 with a balance of 20% equity and 80% bonds. Its great to see the past five years performance (data taken at Dec 2018)

Alternatively, this is most risky fund with a risk level of 5/7 and it is 100% equity or shares. But look at the performance over the past five years (date taken at Dec 2018)

Choose the investment level that you are most comfortable with also remembering that past performance in no way guarantees future performance.

How much to Invest and what fees will you pay?

The next decision to make is how much to invest. You can invest from £100 a month into a Vanguard platform, or start with a one-off £500.

The fees for investing with Vanguard are extremely low and compare very favourably to their competitors. There is an account fee of 0.15%, much lower than most other platforms I have looked at. There will also be a fund charge of between 0.6% and 0.8% which will be deducted from your returns before you receive them. The LifeStrategy funds charge 0.22%. That means that for a £1000 investment, the total cost for one year will only be £3.70 including the cost of the fund and the platform. Investing is not just for the rich!

For an alternative view, go check out Faith Archer’s post on ‘Investing for beginners: Which Vanguard LifeStrategy fund is right for you?’, also in collaboration with Vanguard.

Please be aware that any form of investment can go up and down and you may want to consider advice from a qualified IFA. Just make sure they are recommended by a trusted friend and check their investment levels as some will only work with clients with an investment level of at least £150k. This post was written in collaboration with Vanguard.