So financial admin, a job we all love to hate yes?? But alas there are a few admin jobs that are a must and if you get it right you can save yourself lots of money. A bit of simple planning and organisation will help you to prepare for the future and likely remove some stress and worry. So here’s how to simplify financial admin… the Mrs Mummypenny way !

A few interesting stats

- 40% of UK adults put off organising their day-to-day budget

- More time is spent organising music collections than planning pensions

- 10% of adults don’t review their finances at all

- Of those adults who have lost their pension details, a fifth prefer to live in blissful ignorance

My recommendations for the Key Financial Admin Jobs

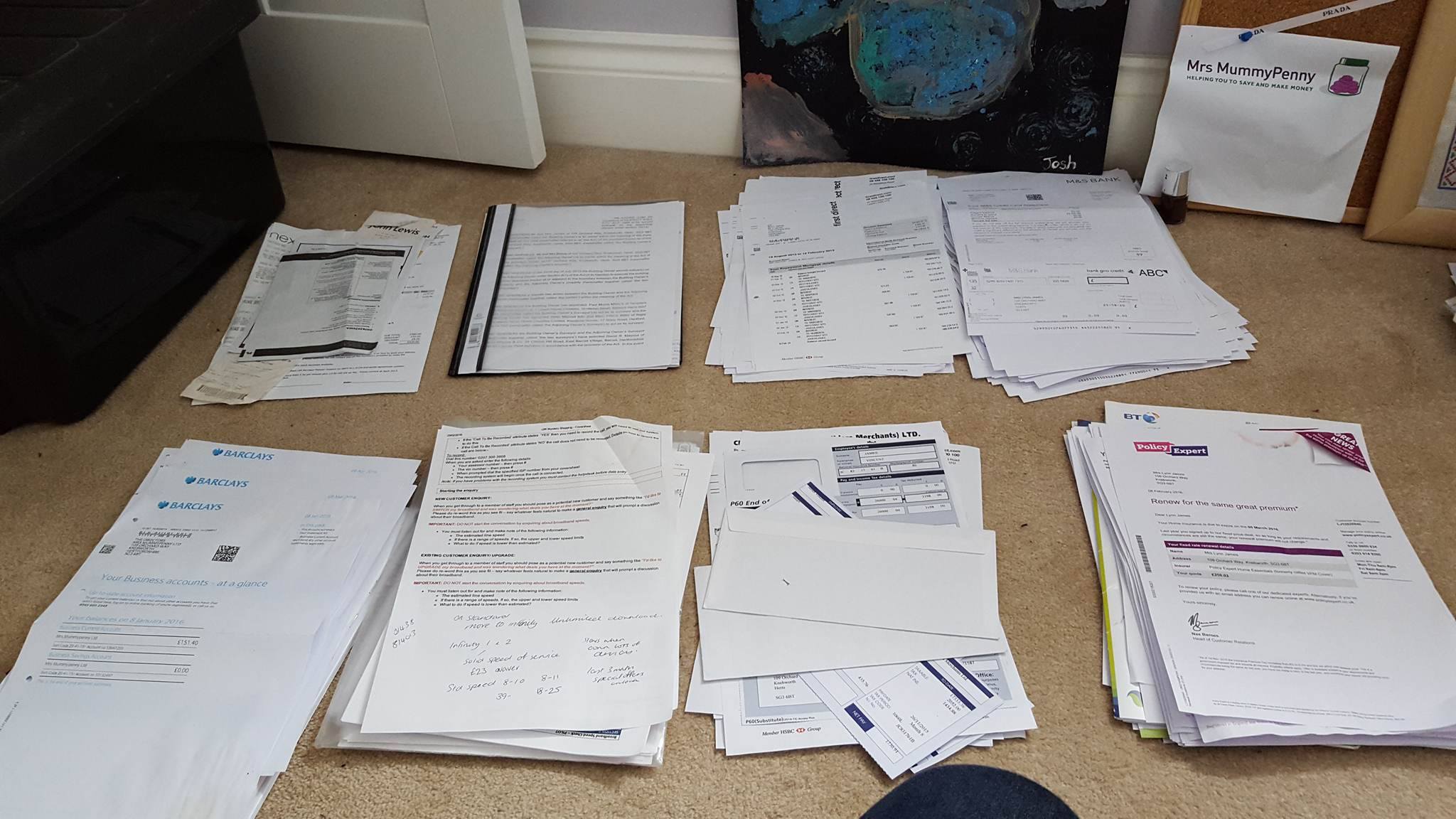

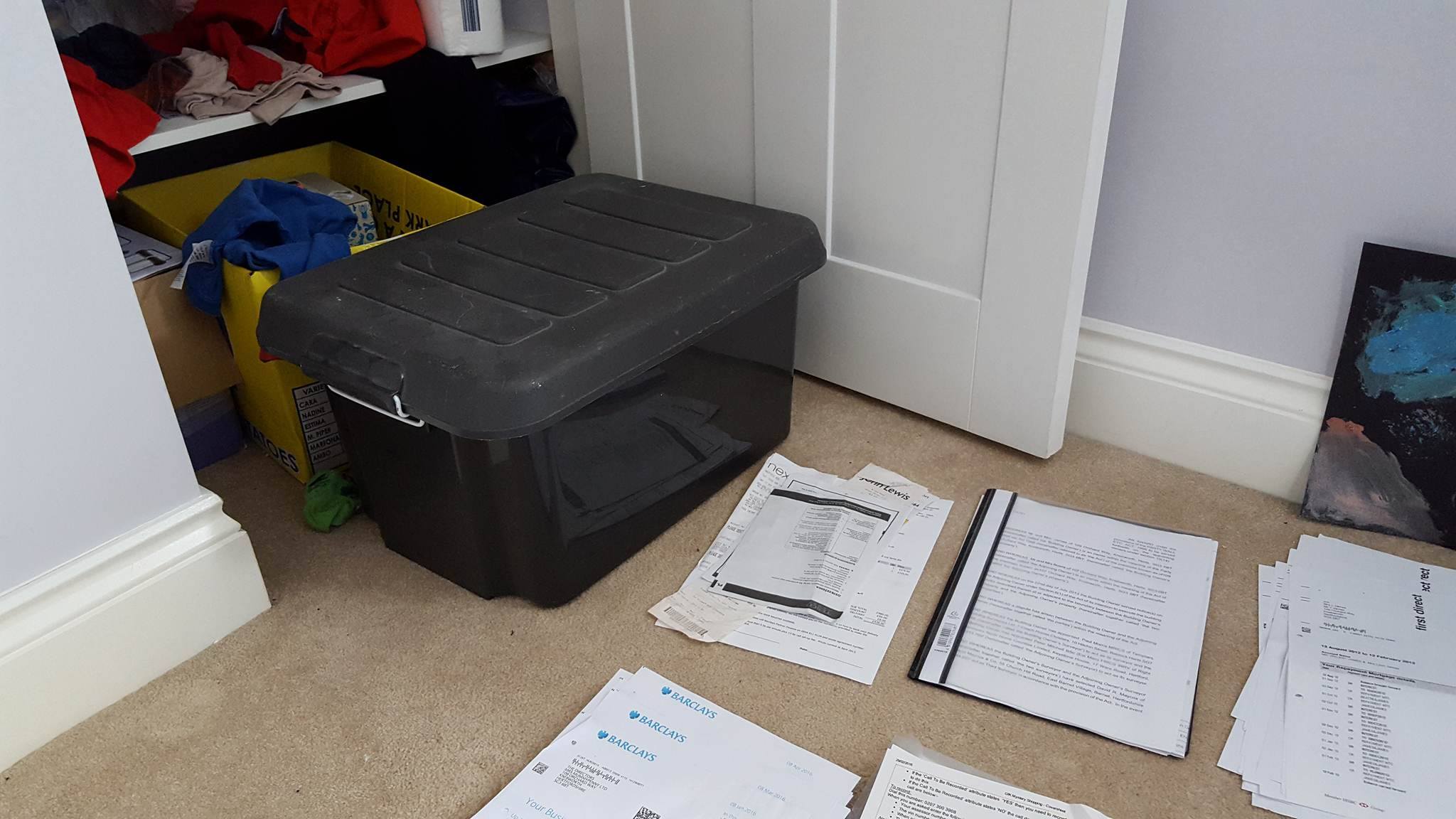

I still get lots of bills/paperwork items in the post even in these ‘digital’ times. I always open my letters every day just in case it’s a cheque 😉 Of course it very rarely is but is sometimes something that needs to be sorted out quickly. So the life lesson here is don’t shove all the unopened post into a drawer! Set aside some time once a month if you bear it, or once every 3 months if not 😉 to go through all the post/paperwork bits that have arrived. And get reading and filing. Here is my spare room at the moment. With piles of paperwork relating to:

- Mrs Mummypenny Paperwork

- Credit card statements

- Household Bills

- Receipts/Instruction manuals

- Personal Tax/Employment stuff

- Current Account/Joint account details

- Savings/Pensions details

- Mortgage Details

Each pile of stuff then gets files in a storage box for when its needed. The other handy benefit of doing this job every month/few months is that it allows to check on a few of the following financial admin jobs:

- Creating a budget. Its very important to know exactly where your money is going every month and that you have enough income to cover your expenditure. Write down a list/create an excel spreadsheet of all your incomings and outgoings. If you need an excel template I have a great one, Email me for a copy. Look through your bank statement for all of your direct debits, credit card charges for your regular costs. It should all be fresh in your head if you have just done your filing.

- Have a good look at all of the outgoings and really think do you need that TV subscription to Netflix or that TV insurance policy? Cancel the stuff you don’t need. Also there are likely to be costs that can be reduced. Is that Sky subscription costing way too much? Can you bear to cancel it? If not call them to threaten you are leaving them, most likely they will offer you a discount. Same goes with your broadband & mobile phone. If your contract is up get on the phone and get that bill reduced 🙂

- Definitely check your utility costs, do a quick comparison check on a site like uSwitch to check you are with the best provider on the best tariff. The first time I did this I save £50 per month!! I urge everyone to do this once a year.

- Check your debt position regularly. Take a look at the paperwork for your latest credit card bills/loans statements/HP agreements and work out how much you owe. It’s a great exercise to carry out and will make you want to do something about it. It is something I do every 6 months. Maybe you are a super lucky person and maybe the only debt you have is a mortgage…that’s not many people I suspect. Anyhow add it up and look at the number written down, if it scares you, you need to do something about it. Are there credit cards with a monthly interest rate that you can swop to a 0% card? There are so many great deals around where you can do a balance transfer. Maybe there is a HP agreement on something that is due to end soon? Result there is some cash soon to be freed up. If you are in a difficult debt position and do not know where to go, please talk to the Citizens Advice Bureau or take a look at Debt camel.

- Add up all your savings pots to hopefully balance out the debts bit above. If you have debt with interest charges swop your savings to pay off your debt. If your debt is low interest/interest free leave things as they are. I have short-term easy access savings and longer term savings. I would advise to have both. I have easy access cash ISA where I will let my spare cash sit, trying to earn a little bit of interest. Unfortunately, interest rates are poor at the moment but do try to maximise where you put your money. I also have an account where I transfer a set amount every month. This is an account where if I make no withdrawals for 12 months I get a nice interest bonus. I am 2 months away from getting a 6% bonus which should be worth around £100. I have a few shares staying locked away until they make some profit 😉 I also invest £25 per month into a shares ISA. I started this 16 years ago and recently cashed in my ISA to help with a house extension and cashed in £5000. Worth it for £25 a month. I also pay small amounts into Child Trust Funds for my children.

- Proper long term savings are your pension. I was not surprised to read that 58% of us don’t review their pensions at all and, of those that do check their private pensions, the average is only once every nine months. Of those adults who have lost their pension details, a fifth (20%) seem unconcerned, preferring to live in blissful ignorance! It is a complicated subject that not a lot of us know much about, including me. All I will say on this is, if like me, you have a few pension pots from different companies you have worked for then keep a record of everything. If you have lost your details then go to https://www.gov.uk/find-pension-contact-details this government link that will help you find it:-) If you don’t have a pension or any other form of longer savings, then get some financial advice from your local friendly financial advisor. Or take a look at a great website like Moneytothemasses who specialises in pensions advice.

Jamie Jenkins, pension expert at Standard Life Savings commented, “Despite the resurgence of vinyl, most music collections will be of limited long term value when it comes to funding retirement. It’s easy to put off things you don’t enjoy but keeping on top of both day-to-day budgeting and longer term savings will help you relax, knowing things are under control for the future. More people than ever have access to a pension through their workplace, and technology is making it easy for people to regularly review their savings online, so there’s no better time than now to get organised.”

Standard Life Savings has put together a book of useful tips and guidance, crowdsourced from consumers and financial experts (including Mrs Mummypenny!), aimed at helping people make the most of their money and get their finances in order. You can view the ‘The Little Guide to Financial Admin’ along with other tips and calculators to help you plan your financial future http://www.standardlife.co.uk/c1/news-and-blog/little-guide-financial-admin/ That’s not all, I will have x copies of the book in paperback version to give away to my wonderful readers. Competition details will be posted on 15th May 2016. Look out for it.

This post was written in collaboration with Standard Life Savings.

5 Responses

The pensions advisory service also gives free pensions guidance and is worth checking out.

Thanks for that added bit of information Karen:-)

Some seriously scary stats at the top of this post! I have to admit I was late to start retirement saving. Playing catch up now and contributing 10% of my wages which I am likely to need to increase again. If only we were taught about the importance of it much younger!

I know its scary numbers. I have a few pensions built up from companies I have worked for..but nothing at present as Im ot earning enough money:-(((. I will soon though. I so wish we were taught about personal finance at school….they do it a bit now, but not enough in my view. MMPx